Imagine a world where countries, or groups of countries, become increasingly isolated leading to a multipolar(ised) world. The infrastructure industry is dominated by domestic champions that are slow to innovate and slow to adapt to external shifts, such as climate change

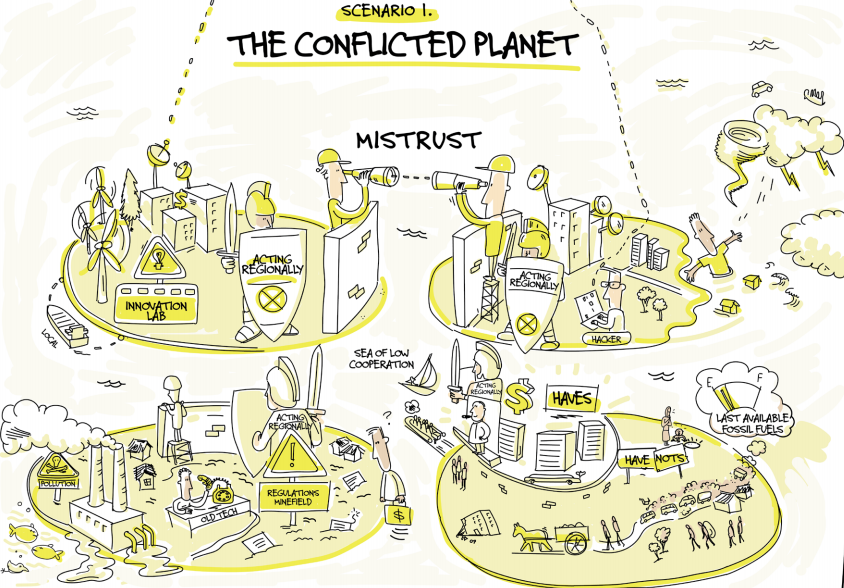

The first of three hypothetical scenarios designed by the Global Infrastructure Hub, The Conflicted Planet, is defined by:

- Geopolitical context (multipolar)—Heightened global political competition leads to a reliance on local markets and the formation of regional trade blocs. The infrastructure industry becomes dominated by monopolistic companies with deep connections to government.

- Pace of climate change (rapid)—The world moves at multiple speeds to tackle climate change with some regions seeking to mitigate impacts, while others pursue adaptation-based strategies. The infrastructure industry, now increasingly domestic, aligns with domestic climate policy.

- Technological progress (incremental)—Incremental development and uptake of new technology hinders productivity growth and climate responsiveness across economies. The infrastructure sectors are acutely impacted as productivity gains lag other sectors.

The structure of international cooperation is multipolar and defined by regional allegiances. Geopolitical rivalry shapes all forms of political and economic interactions (domestic and international).

Trade becomes politically motivated, rather than following comparative advantage, leading to significant cost inefficiencies in domestic economies. Local economies increasingly rely on local (and regional) factor markets to retain local jobs that might otherwise be lost in a system of open, global trade (for example, a reduction in the offshoring of technology and manufacturing jobs).

Many nations design economic policy to project a strong outward image, resulting in a bias toward monopolistic national champions. These national champions rely on interventionist policies to erect artificial barriers to competition and to provide strategic funding support.

In nations where governance norms are not well established, the risk exists that domestic inequality may increase due to the concentration of rents among the beneficiaries of powerful domestic monopolies. On the other hand, nations (and regions) with entrenched governance norms may actually see inequality fall as firms (and governments) increasingly rely on local labour and product markets.

Regionalisation drives local regulatory harmonisation, creating a global economy characterised by a tapestry of regulatory, governance and cooperation systems across regions.

Different regions pursue markedly different climate strategies despite the rapid pace of climate change. Some regions take progressive stances by attempting to mitigate climate impacts through incentives programs designed to spark innovation in climate-smart technology, and to transition to renewable power. Other regions are less concerned with climate change, preferring to optimise the economy for short-term growth and employment. The lack of unified climate policy negatively impacts the geographically disadvantaged, and especially the economically disadvantaged in relatively poorer regions, who are highly

exposed to the adverse impact of weather-related events. Over time, the shifting climate may increase the number of climate-displaced peoples.

The pace of technological progress is incremental. The diffusion of technology is limited with national champions hoarding intellectual property and stymying technological innovations by domestic competitors. Lackluster technological development, combined with anticompetitive market structures, slows innovation and productivity gains. The general lack of innovation incentives and frequency of state interventions leads to an infrastructure market that relies on public funding streams.

Change in infrastructure business models

This scenario sees the infrastructure industries shift in orientation and market structure. A once globalised and competitive business becomes domestically oriented and monopolistic (with regulations barriers and public financial support creating artificial barriers to entry). National champions may vertically integrate across sector value chains or scale to the size of large, national holding companies integrating multiple strategic sectors. Given the anti-competitive market structures and limited technological innovation, these

champions operate with limited commercial incentives and the political mandate to maximise employment opportunities.

The inherent strength and sophistication of domestic factor markets (labour, capital, technology, building materials) act as fixed constraints on the scale (and capacity) of the national infrastructure champions. Regulatory harmonisation enables firms to compete within regions and, to the extent possible, draw on regional factor markets. It is expected that the relative scarcity of resources encourages coordination within regional blocs, particularly in the water, power generation and building materials sectors.

International infrastructure cooperation (in terms of sharing knowledge, capital and resources) slows despite continued cooperation within some regional blocs.

The transnational transport and logistics sectors are the most adversely affected. The reduction in

international trade negatively impacts shipping-related industries; shifts patterns of air travel and reduces the attractiveness of air-related assets; and shifts the importance of port-hinterland connections. The travel and logistics industry are constrained by the scale of domestic demand, unless a region establishes a robust trading system, with significant specialisation in last-mile, intra-urban logistics expected.

The globalised private and public financial markets for infrastructure reduce in importance. Nations with established savings pools, mature capital markets and sophisticated banking institutions continue to pursue private participation agendas shaped by national champions in the financial and infrastructure industries.

The transnational private participation market stalls, however, with limited cross-boundary activity (financial or operational) between regional blocs.

Rise in national security infrastructure

In a world where the national strategic interest is paramount, governments invest heavily in sectors viewed as essential for security: energy, water, telecommunications and cybersecurity.

Regional blocs are focused on some degree of regulatory alignment to enable formation of regionalised internets that amplify the national interest and limit the flow of information across global regions.

Cybersecurity for the telecommunications and energy sectors becomes imperative, in particular the security and ongoing maintenance of data centres or hubs.

The scale of investment into social sectors, such as education and healthcare, varies significantly across

countries.

Utility sectors and power and water take precedence, with nations attempting to satisfy domestic demand from local factor markets.

Vertically integrated national power and water markets are common with power feedstocks and water serving as foundational coordination mechanisms in regional blocs (to overcome domestic resource constraints).

Emerging nations with limited resource endowments allow foreign champions to provide basic services from electricity to water and telecommunications, requiring the champions to absorb significant costs related to regulatory alignment, and administrative costs linked to establishing foreign presence.

The fiscal burdens are large to support these strategically essential sectors. The vertical integration of the sectors drives economic inefficiencies exacerbated by highly bureaucratic institutions. The state subsidises basic services to manage domestic inequality.

Public infrastructure investment re-prioritised

Rapid progression of climate change does not serve to galvanise coordinated global action. Countries and regions pursue divergent strategies with varying degrees of coordination within regional blocs. However, improving the resilience of national infrastructure stocks is a cross-cutting priority. This is likely to have three broad impacts.

First, improving resilience leads to innovations in the building materials sectors. The innovations target materials capable of resisting the intensification of climatic events, or, more likely, process improvements capable of reducing the cost of producing the engineered materials needed to restore asset operations in the case of a severe weather event.

Second, the infrastructure industry is likely to develop more modular ways of constructing and expanding assets in a more climatically volatile world. This agility will enable planners to not only respond after an event, but also to rapidly scale, or retrench, capacity across other parts of the asset networks to manage second- and third-order impacts. Fundamentally, this will mean that the design phase of the

project life cycle is commoditised once modular designs are tested and rolled-out, thereby creating significant first-mover advantages for the asset design industry.

Third, the shift to more modular designs, agile network planning and the use of advanced building materials will be complemented by technological innovations. Advanced digital twins covering the full duration of an asset’s life (from conceptualisation through operation) and advanced analytics to manage the functioning of critical asset networks are likely to be deployed. These tools will enable planners to forecast impacts on asset networks (including changes in demand) and develop remedial solutions.

These changes may be more muted in emerging markets. Technological diffusion is likely to be limited unless significant concessions are granted on market access, competition, factor market access, and political allegiance. This is likely to create powerful incentives for domestic innovation, provided national champions do not crowd out smaller firms, as emerging nations seek domestic solutions to combat the changing climate.

Limited global coordination

The reorientation of the infrastructure industries toward local monopolies (depending on sector and location on the value-chain) reduces the importance of multilateral cooperation.

Common practices in project preparation, procurement best practices, shared expectations on construction standards, and sophistication of asset management post-construction either regionalise or dissipate.

Global coordinated action against poor governance practices and wasteful spending are also less common as national governments exert ‘national interest’ narratives over the domestic infrastructure industry.

Environmental legislation, including carbon emission targets and sustainability standards, vary significantly across regions reflecting national (or regional) priorities. Those nations with the financial ability, political alignment and risk exposure improve the resilience of existing infrastructure assets in the face of increasingly frequent and intense natural disasters. While some intra-regional cooperation is expected on environment protection and climate change adaption (and mitigation), the scale is limited to those regions facing the greatest risk from shifts in weather events.

The erosion of multilateral fora to tackle global challenges has second- and third-order impacts on socioeconomic issues, particularly for emerging nations that benefitted from the financing and expertise available from the deceased international financial institutions.

This scenario has been taken from the Global Infrastructure Hub’s Infrastructure Futures report. The scenarios offer deliberately extreme, yet plausible, versions of the future. They are not predictions, but are instead designed to prompt debate and encourage members of the infrastructure community

to investigate the potential impacts and implications of these scenarios, and take action to ensure their strategies and plans are resilient to the full range of possible developments.

Keep an eye out for Scenario Two coming next week.